Autonomous Train Market Size, Share & Industry Analysis, By Grade of Automation (GoA) (GoA1 (Manual Operation), GoA2 (Semi-Automated), GoA3 (Driverless), and Others), By Train Type (Metro/Urban Transit, High-Speed Rail, Freight Trains, and Others), By Component (Rolling Stock (Trains), Signaling & Train Control Systems, Communication Systems, Software & AI Systems, and Others), By Automation Technology (CBTC (Communication-Based Train Control), ETCS (European Train Control System), and Others), By Application (Passenger Transport and Freight Transport), and Regional Forecast, 2026–2034

Autonomous Train Market Overview

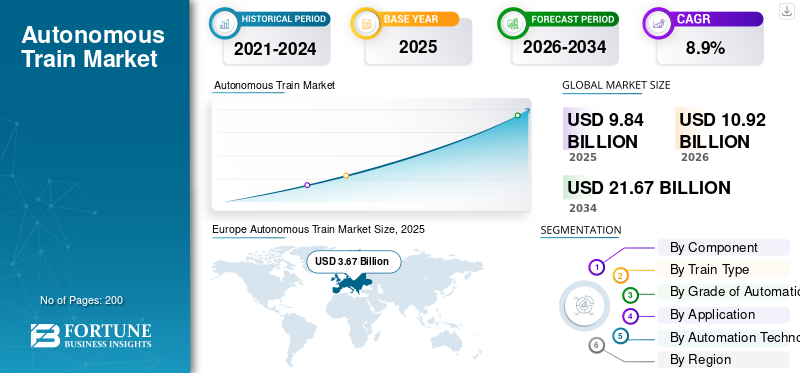

The global autonomous train market size was valued at USD 9.84 billion in 2025. The market is projected to grow from USD 10.92 billion in 2026 to USD 21.67 billion by 2034, exhibiting a CAGR of 8.9% during the forecast period.

An autonomous train is a rail system that operates with minimal or no human intervention using advanced sensors, control systems, and automation technologies to ensure safe and efficient rail transport. Market growth is driven by rising demand for efficient public transportation, increasing investments in rail infrastructure, advancements in autonomous technologies, and the adoption of predictive maintenance solutions, all of which improve safety and operational efficiency.

Major players in the market include Siemens Mobility, Alstom, Hitachi Rail, Thales Group, CRRC Corporation Limited, and Wabtec Corporation, competing through advanced train technology, digital signaling systems, AI-driven automation, and integrated rail infrastructure solutions.

Download Free sample to learn more about this report.

AUTONOMOUS TRAINS MARKET TRENDS

Rising Adoption of AI-Enabled Predictive Maintenance is Transforming the Global Market Trend

The integration of artificial intelligence and predictive maintenance is transforming trends in the global autonomous train market. Rail operators are increasingly deploying smart monitoring systems to track component health in real time, reducing unexpected failures and maintenance costs. This trend supports improved safety, reliability, and lifecycle management of rail systems. As digitalization expands across rail infrastructure, predictive analytics is becoming a core element of autonomous train technology, enabling efficient scheduling, minimizing downtime, and strengthening overall transportation system performance.

- In April 2026, SMRT partnered with Oracle to deploy an AI-enabled rail maintenance platform using Oracle Cloud Infrastructure and Autonomous AI Database. The JARVIS system leverages predictive maintenance, real-time analytics, and machine learning to enhance rail reliability, safety, and operational efficiency.

Expansion of Metro Lines and Urban Rail Systems Accelerates Automation Demand

Rapid urbanization and increasing congestion are driving investments in metro lines and urban rail systems globally. Governments are prioritizing automated and driverless trains to improve public transportation efficiency and reduce human dependency. This trend is particularly visible in the Asia Pacific autonomous train market, where large-scale infrastructure projects are underway. The expansion of smart cities and integrated transportation systems is further supporting the deployment of autonomous systems, enhancing the passenger experience while ensuring high-frequency, reliable rail transport services.

- In April 2026, Alstom secured a contract to deliver 39 driverless trainsets for Mumbai Metro Line 4, integrating CBTC signaling from Larsen & Toubro to enhance automation, safety, and operational efficiency, and to support India’s transition toward advanced autonomous urban rail systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Safe and Efficient Public Transportation Drives Market Growth

The growing need for safer, faster, and more reliable public transportation systems is a key driver for the global autonomous train market growth. Autonomous technologies help minimize human errors, enhance operational precision, and improve passenger safety. Rising urban population and daily commuting needs are pushing governments to modernize rail systems. As a result, autonomous train systems are being widely adopted to ensure efficient transportation, reduce delays, and support large-scale passenger movement across major cities and regions.

- In July 2026, Mumbai Metro Line 4 advanced its automation plans with Alstom supplying driverless trains and Larsen & Toubro deploying CBTC signaling, enhancing real-time monitoring, passenger safety, service frequency, and supporting India’s shift toward modern autonomous rail transport systems.

Government Investments in Advanced Rail Infrastructure Fuel Market Expansion

Strong government support and funding for upgrading rail infrastructure are significantly driving demand for the global autonomous train market. Investments in signaling systems, communication networks, and automated control technologies are enabling the transition toward fully autonomous rail transport. Countries across Europe, North America, and the Asia Pacific are focusing on modernizing existing rail systems and developing new high-speed and metro networks. These initiatives are accelerating the deployment of autonomous technology and strengthening the overall transportation ecosystem.

- In March 2026, Poland initiated testing of an autonomous train under a PKP-led consortium, deploying ATO-based systems on a commuter line near Warsaw, using AI, sensors, and digital twin simulations to enhance passenger rail automation and operational safety.

MARKET RESTRAINTS

High Initial Infrastructure Costs Limit Widespread Adoption

One of the major restraints in the global autonomous train market is the high capital investment required for infrastructure development and system integration. Deploying autonomous systems involves significant costs related to advanced signaling, communication systems, and track modernization. Additionally, upgrading legacy rail infrastructure to support automation can be complex and expensive. These financial barriers may slow down adoption, particularly in developing regions where budget constraints and competing infrastructure priorities limit large-scale investments in autonomous technologies.

MARKET OPPORTUNITIES

Integration of Autonomous Technologies in Freight Rail Opens New Revenue Streams

The adoption of self-driving train technology in freight rail presents significant growth opportunities. Automation can enhance efficiency in cargo movement, reduce operational costs, and improve scheduling accuracy. Freight operators are increasingly exploring driverless train solutions to optimize long-haul and heavy-load transportation. This shift supports better utilization of rail systems and reduces dependency on manual operations. As global trade expands, the integration of autonomous technologies into freight transportation is expected to create new revenue opportunities.

- In July 2025, DP World, Deendayal Port Authority, and Nevomo signed an MoU to pilot autonomous MagRail freight technology in India, enabling electric, self-propelled cargo wagons to enhance port efficiency, reduce emissions, and modernize rail-based logistics operations.

Advancements in Digital Signaling and Communication Systems Enable Market Opportunities

Continuous technological advancements in digital signaling, communication-based train control, and real-time monitoring systems are creating strong opportunities in the autonomous train market. These innovations enable seamless coordination between trains, tracks, and control centers, enhancing overall system efficiency. The adoption of cloud computing, IoT, and AI is further supporting the development of intelligent rail systems. As rail operators aim to improve safety and operational performance, these advancements are opening new avenues for innovation and long-term market growth.

- In July 2024, Alstom signed a USD 3.28 billion framework contract with Hamburger Hochbahn to supply up to 374 metro trains and CBTC signaling for Hamburg’s U5 line, enabling fully and semi-automated operations with high-frequency driverless services.

MARKET CHALLENGES

Cybersecurity Risks and System Reliability Concerns Pose Key Challenges

As autonomous systems in rail rely heavily on digital technologies and interconnected networks, cybersecurity and system reliability have become critical challenges. Potential cyber threats can disrupt operations, compromise passenger safety, and impact public trust. Ensuring secure communication and data protection across rail systems is essential for smooth functioning. Additionally, maintaining consistent system performance under varying operational conditions requires robust testing and validation. Addressing these challenges is crucial for the sustainable growth of the global autonomous train market.

Segmentation Analysis

By Component

Advanced Signaling Infrastructure and Automation Needs Drive Signaling & Train Control Systems Segment Growth

Based on component, the market is segmented into rolling stock (trains), signaling & train control systems, communication systems, software & AI systems, and integration & services.

The signaling & train control systems segment dominates the market due to its critical role in enabling safe and efficient train operations. These systems ensure real-time train monitoring, collision avoidance, and optimized traffic management. Increasing investments in rail infrastructure modernization and deployment of driverless trains across metro lines continue to sustain strong demand for advanced signaling technologies globally.

- In September 2024, European rail initiatives advanced ATO over ETCS deployment, demonstrating interoperable GoA2-GoA4 automation systems that enhance rail capacity, improve energy efficiency, optimize scheduling, and support wider adoption of autonomous technologies across diverse rail networks.

The software & AI systems segment is projected to grow at a 11.0% CAGR during the forecast period. Rising adoption of AI-driven automation, predictive maintenance, and real-time data analytics is accelerating demand, enabling smarter decision-making and enhanced performance of autonomous systems.

By Train Type

High Urbanization and Smart City Expansion Propel Metro/Urban Transit Segmental Growth

Based on train type, the market is segmented into metro/urban transit, high-speed rail, freight trains, and light rail & monorail.

The metro/urban transit segment dominates the market due to its extensive deployment in densely populated cities and strong alignment with public transportation needs. Increasing investments in metro lines, smart city projects, and automated rail systems are driving adoption. High passenger volumes and the need for frequent, reliable services further accelerate the integration of autonomous systems in urban environments.

- In September 2023, Alstom delivered advanced CBTC-enabled metro trainsets for India’s Bhopal-Indore smart city project, featuring automated operations, energy-efficient systems, and high-capacity design, supporting sustainable urban mobility and modernization of public transportation infrastructure.

The freight trains segment holds the second-largest share and is projected to grow at a CAGR of 6.1% during the forecast period. Growing demand for efficient cargo transportation, long-haul logistics optimization, and automation in rail freight operations is supporting the steady adoption of autonomous technologies.

To know how our report can help streamline your business, Speak to Analyst

By Grade of Automation (GoA)

Operational Flexibility and Gradual Automation Adoption Drive GoA2 (Semi-Automated) Development

Based on grade of automation (GoA), the market is segmented into GoA1 (manual operation), GoA2 (semi-automated), GoA3 (driverless), and GoA4 (unattended train operation).

The GoA2 (Semi-Automated) segment holds the largest autonomous train market share due to its balance between automation and human control, allowing operators to enhance efficiency without fully overhauling existing rail systems. It is widely adopted across established rail networks, as it enables improved safety, optimized operations, and easier integration with legacy rail infrastructure.

- In February 2026, Switzerland’s Waldenburg Railway introduced semi-automated GoA2 train operations using Stadler’s CBTC system, enhancing efficiency, safety, and punctuality while advancing digital rail control and preparing for future fully autonomous train deployment.

The GoA4 (unattended train operation) segment is expected to grow at a CAGR of 11.0% during the forecast period. Increasing deployment of fully autonomous metro systems, rising investments in smart rail infrastructure, and demand for driverless trains are accelerating adoption globally.

By Application

Rising Urban Mobility Needs and High Passenger Volume Propel Passenger Transport Segment

Based on application, the market is segmented into passenger transport and freight transport.

The passenger transport segment dominates the market due to increasing reliance on rail-based public transportation systems in urban areas. High passenger volumes, expansion of metro lines, and growing adoption of self-driving train systems to enhance safety and efficiency are driving demand. Governments are prioritizing smart mobility solutions, further accelerating the deployment of driverless trains in urban transit networks.

- In April 2026, Czechia launched Europe’s first driverless passenger train on the Kopidlno–Dolní Bousov line, using sensor-based autonomous systems under testing, marking a milestone in rail automation with plans for fully unattended operations by 2031.

The freight transport segment is projected to grow at a CAGR of 7.4% during the forecast period. Increasing demand for efficient cargo movement, long-distance logistics optimization, and automation in rail operations is supporting the steady adoption of self-driving technology.

By Automation Technology

Advanced Communication Systems and Urban Rail Automation Drive CBTC Segment Growth

Based on automation technology, the market is segmented into CBTC (communication-based train control), ETCS (European Train Control System), PTC (positive train control), and others.

The CBTC segment dominates the market due to its widespread adoption in metro lines and urban rail systems, enabling real-time communication, improved train frequency, and enhanced safety. Its ability to support fully autonomous systems and optimize rail transport operations is driving strong demand across modern rail infrastructure projects globally.

- In August 2025, Alstom partnered with Larsen & Toubro to deliver driverless metro trains and CBTC signaling for Mumbai Metro Line 4, enhancing urban rail connectivity, supporting sustainable transportation, and enabling fully automated GoA4 operations with integrated maintenance services.

The ETCS segment holds the second-largest share and is projected to grow at a CAGR of 9.7% during the forecast period. Increasing standardization of rail systems across Europe and ongoing upgrades in cross-border rail infrastructure are supporting the adoption of ETCS technologies.

Autonomous Trains Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa

Asia Pacific

Europe Autonomous Train Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific represents the second-largest and fastest-growing region, projected to grow at a CAGR of 10.7% during the forecast period. Rapid urbanization, increasing population density, and large-scale investments in metro lines and rail infrastructure are driving demand. Countries such as China, India, and Japan are actively deploying self-driving systems to enhance public transportation efficiency. Government-led smart city initiatives and advancements in autonomous technologies are further strengthening the region’s growth trajectory.

- In September 2024, JR East announced plans to launch self-driving trains on the Joetsu Shinkansen by 2028, gradually advancing from GoA2 to fully autonomous operations, enhancing efficiency, sustainability, and innovation in high-speed rail transport systems.

China Autonomous Trains Market

The Chinese market in 2026 is estimated to be USD 1.95 billion, accounting for roughly 17.9% of the global revenues. Strong government investments in metro lines, high-speed rail, and autonomous technologies drive dominance, supported by rapid urbanization.

Japan Autonomous Trains Market

The Japanese market in 2026 is estimated to be USD 0.45 billion, accounting for roughly 4.1% of the global market revenues. Advanced rail systems, technological advancements, and a focus on safety and efficiency support steady growth.

India Autonomous Trains Market

The Indian market in 2026 is estimated to be USD 0.46 billion, accounting for roughly 4.2% of the global market revenues. Rapid urban expansion, metro projects, and smart rail infrastructure investments drive the fastest growth trajectory.

North America

North America holds the third-largest share in the global market, driven by ongoing upgrades to aging rail infrastructure and increasing focus on safety and efficiency. The U.S. and Canada are investing in advanced signaling systems, positive train control technologies, and automation solutions to enhance rail transport operations. Growing interest in predictive maintenance and digital rail systems is supporting adoption. However, gradual implementation and regulatory complexities moderate the pace of self-driving train deployment.

- In April 2025, Parallel Systems launched its first autonomous rail pilot in Georgia, deploying battery-electric railcars on a 160-mile route, enhancing freight efficiency, reducing road congestion, and advancing the commercialization of autonomous rail transport technologies.

U.S. Autonomous Trains Market

The U.S. market in 2026 is estimated to be USD 1.77 billion, accounting for roughly 16.2% of the global autonomous train market revenues. Focus on safety, predictive maintenance, and upgrading aging rail infrastructure supports steady adoption.

Europe

Europe holds the largest market share in the global market due to its well-established rail infrastructure and early adoption of self-driving train technology. Countries such as Germany, France, and the U.K are investing heavily in modernizing rail systems and expanding high-speed and metro networks. Strong regulatory frameworks, focus on sustainable public transportation, and widespread deployment of driverless trains across urban transit systems continue to support steady market growth across the region.

- In September 2025, Futurail secured USD 8.8 million in funding to develop an AI-driven autonomy stack for self-driving trains, supporting Europe’s shift from road to rail by improving efficiency, reducing costs, and enhancing sustainable rail transport capacity.

Germany Autonomous Trains Market

The German market in 2026 is estimated to be USD 0.75 billion, accounting for roughly 6.9% of global market revenues. Strong rail infrastructure, automation adoption, and modernization initiatives support consistent market expansion.

U.K. Autonomous Trains Market

The U.K. market in 2026 is estimated to be USD 0.55 billion, accounting for roughly 7.3% of global market revenues. Increasing investments in digital rail systems and the modernization of public transportation networks drive growth.

South America

South America is gradually adopting self-driving systems, supported by growing investments in rail transport infrastructure. Countries such as Brazil and Argentina are focusing on improving urban mobility and freight efficiency through modernization projects. Increasing demand for reliable public transportation and expansion of metro networks are contributing to market growth. While adoption remains at an early stage, improving economic conditions and government initiatives are expected to drive steady progress in autonomous technology deployment.

- In January 2026, Alstom and Santiago Metro unveiled the first fully automated Metropolis train for Line 7 in Chile, featuring advanced onboard systems, high passenger capacity, and driverless operation to enhance urban rail efficiency and public transportation experience.

Middle East & Africa

The Middle East & Africa region holds the fourth-largest share, driven by increasing investments in smart city projects and modern rail systems. Countries such as the UAE and Saudi Arabia are deploying advanced metro and rail networks incorporating autonomous technologies. The focus on enhancing public transportation, reducing congestion, and supporting sustainable mobility is accelerating adoption. Additionally, large-scale infrastructure projects and international partnerships are contributing to the gradual expansion of self-driving train systems in the region.

- In November 2024, Riyadh inaugurated its fully automated metro network with six lines, marking a major milestone in smart urban mobility, enhancing public transportation efficiency, supporting sustainability goals, and advancing large-scale driverless rail system deployment under Vision 2030.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Automation, Digital Signaling, and Strategic Partnerships Define Competitive Landscape

The market is moderately consolidated, with a mix of global technology providers and regional rail solution companies competing for market share. Key players such as Siemens Mobility, Alstom, Hitachi Rail, Thales Group, CRRC Corporation Limited, and Wabtec Corporation compete through advanced self-driving train technology, digital signaling systems, and integrated rail infrastructure solutions. Companies are focusing on AI-driven automation, predictive maintenance, and software-based control platforms to enhance efficiency. Strategic partnerships, long-term rail contracts, and investments in smart transportation systems strengthen their competitive positioning across global markets.

- In October 2025, CRRC unveiled the world’s first driverless train capable of reaching 200 km/h, featuring advanced sensors, smart diagnostics, and energy-efficient design, marking a major breakthrough in high-speed autonomous rail technology and safety innovation.

LIST OF KEY AUTONOMOUS TRAIN COMPANIES PROFILED

- Siemens Mobility (Germany)

- Alstom SA (France)

- Hitachi Rail (Japan)

- Thales Group (France)

- CRRC Corporation Limited (China)

- Wabtec Corporation (U.S.)

- Mitsubishi Heavy Industries (Japan)

- Kawasaki Heavy Industries (Japan)

- Stadler Rail AG (Switzerland)

- CAF (Construcciones y Auxiliar de Ferrocarriles) (Spain)

- Hyundai Rotem (South Korea)

- Toshiba Infrastructure Systems & Solutions (Japan)

- Knorr-Bremse AG (Germany)

- Ansaldo STS (Hitachi Rail STS) (Italy)

- ABB Ltd. (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Ho Chi Minh City is set to receive its first driverless metro trains from Hyundai Rotem, enhancing urban rail systems with faster, safer, and more sustainable public transportation while supporting the modernization of metro lines and autonomous train adoption.

- October 2025: Siemens Mobility unveiled a driverless Mireo electric train with ETCS, ATO, and sensor-based obstacle detection, advancing GoA4 automation, enhancing safety, reducing operational costs, and supporting the digital transformation of rail transport systems.

- July 2025: Hitachi Rail and DB Cargo launched Europe’s first automated freight locomotive equipped with ATO and remote operation technologies, enhancing rail capacity, energy efficiency, and advancing the shift toward fully autonomous freight rail systems.

- July 2025: China launched its first autonomous rail yard at Suxi terminal, integrating automated cranes, intelligent transport systems, and digital logistics platforms to enhance efficiency, reduce costs, and support smart, low-carbon freight transportation networks.

- May 2025: RTRI developed an advanced autonomous train operation system enabling onboard decision-making, obstacle detection, and control of rail infrastructure, improving safety, reducing workforce requirements, and advancing fully automated train operations.

- April 2025: AŽD demonstrated an autonomous passenger train operating in open landscapes in Czechia, using AI, lidar sensors, and real-time data systems, marking a breakthrough in autonomous rail deployment beyond controlled urban environments.

- April 2024: Copenhagen announced plans to deploy fully autonomous trains by 2030, with Siemens Mobility providing CBTC and GoA4 systems to enhance rail capacity, reduce energy consumption, and modernize urban public transportation infrastructure.

- June 2023: Europe’s Rail launched the USD 188.5 million FP2 R2DATO project to advance digital and automated railways, aiming to achieve scalable autonomous train operations up to GoA4, improve infrastructure capacity, and enhance sustainable rail transport efficiency across Europe.

REPORT COVERAGE

The global autonomous trains market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.9% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Component, By Train Type, By Grade of Automation (GoA), By Application, By Automation Technology, and By Region |

| By Component |

|

| By Train Type |

|

| By Automation Technology |

|

| By Grade of Automation (GoA) |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.84 billion in 2025 and is projected to reach USD 21.67 billion by 2034.

In 2025, the European market value stood at USD 3.67 billion.

The market is expected to exhibit a CAGR of 8.9% during the forecast period.

The metro/urban transit segment leads the market by train type.

Government investments in advanced rail infrastructure fuel market expansion.

Major players in the market include Siemens Mobility, Alstom, Hitachi Rail, Thales Group, CRRC Corporation Limited, and Wabtec Corporation.

Europe holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us